Retail Chronicles | 25.01.2021

Retail Chronicles | 25.01.2021

Emerging trends in retail and new commerce.

Hello, it’s Laurent from Spring Invest, a French investment fund that is shaping the future of commerce. Welcome to the latest edition of Retail Chronicles, our bi-monthly newsletter about emerging trends in (e-)retail, brands, and new commerce.

🔮 2021 trends

January is a traditional time for predictions for the year to come. Even if the COVID-19 context does not make it easy, current deal flow and our interactions with retailers and e-merchants can shed light on some 2021 trends:

Omnichannel as a new normal: omnichannel businesses have shown great resilience in 2020; from small stores to large retailers, from small brands to large e-commerce players, omnichannel is a strategic issue that will mobilize important operational and technical resources (unification of information system - CRM, ERP, WMS, standardization of data, full digitization of stocks, the transformation of supply chains…).

Direct-to-consumer strategy: brands should probably accelerate their direct-to-consumer distribution strategy.

Logistics is booming as we said in a previous newsletter. The sector should face many issues :

Maintaining efficiency while sales volume are drastically increasing;

Optimizing delivery strategy, especially for large cities (last-mile fulfillment centers, dark stores, local pick-up…);

Revers logistics;

Value-added services to e-merchants logisticians ;

Digitalization of processes (upstream and downstream supply chains);

Mechanization or automation of warehouses.

Retail Digital Media: trends began in 2020 with an increasing budget in digital media, driven by regulatory and environmental issues, and growing interest for drive-to-store solutions; new habits of retailers and brands using more and more digital media providing better reach and KPIs will probably remain in 2021;

Customer acquisition and retention strategy:

Influence marketing and how to create and manage a community to establish elements of trust ;

Social network-related commerce: Instagram, TikTok…;

Live/video shopping;

Customer engagement (as people are less visiting physical stores, are chatbot or AI the right solution ?).

Circular economy:

Second-hand products : Because of the Covid Crisis, consumers should pay more and more attention to their budget which should accelerate the second-hand market;

Reconditioning: e-commerce is growing fast increasing return logistics issues and the need for dedicated channels to sell those products.

Make or buy : environmental (sustainable approach), business (reducing the time of production or repair) and technological issues (technologies such as 3D printing are now more mature) may enhance the maker trends.

Cybersecurity issue: (e-)retailers are still facing many threats (payment fraud, e-commerce tag hacking,…).

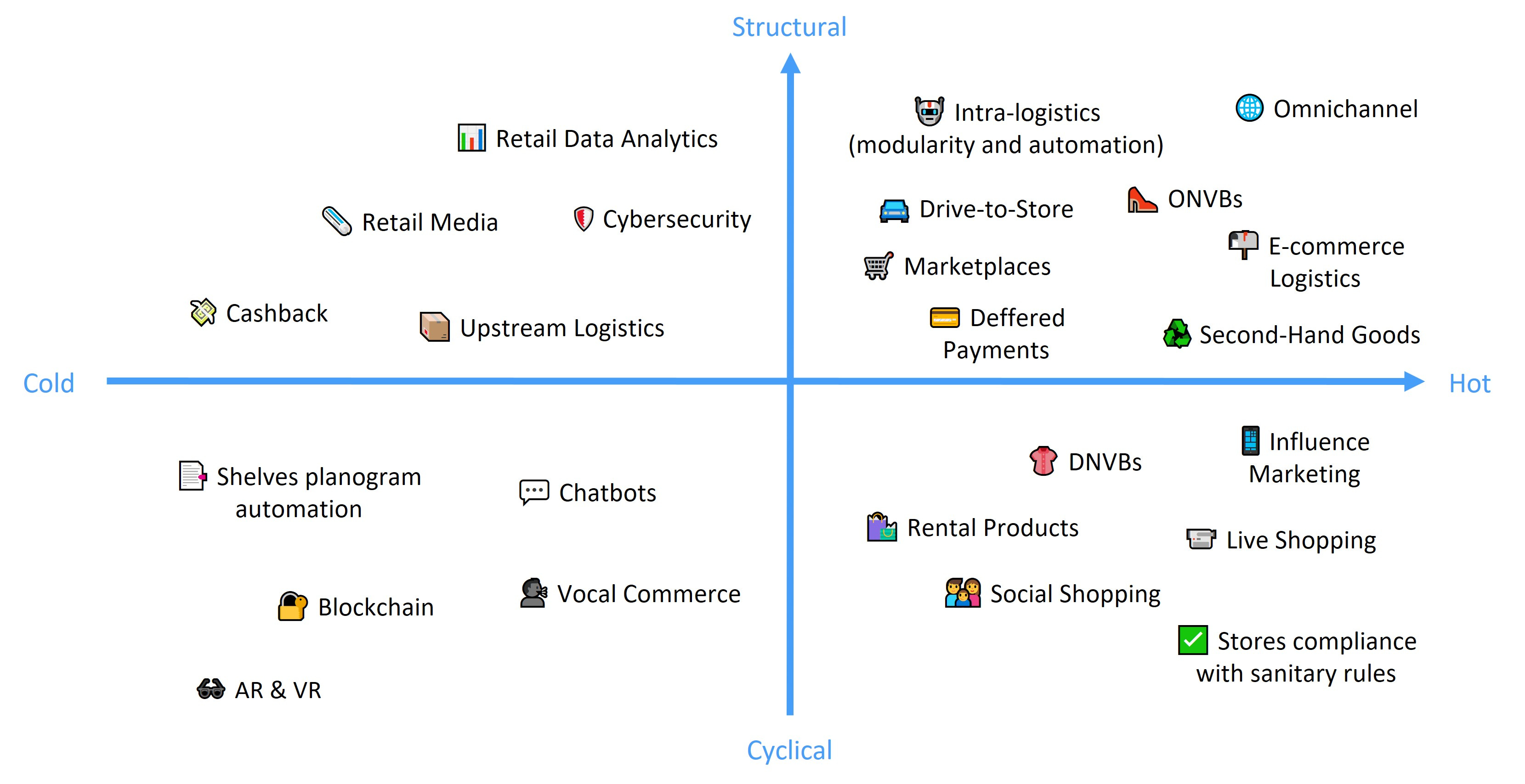

At Spring Invest, we are used to differentiating structural innovation (for solid foundations) from cyclical innovation depending on market trends. The following Heatmap tries to summarize some of the topics we are currently looking at:

🚚 Return logistics is the new challenge for e-merchants

Driven by the e-commerce growth, logistics is another market segment that performed particularly well in this period. Return logistics is becoming a real operational issue for logisticians and a great opportunity for liquidators and resellers.

In this paper from Michael Waters, we learn that (i) 15% to 40% of goods bought online are returned (vs 5-10% for in-store purchase and (ii) 25% of returns are thrown out on average, products being damaged or unusable.

E-merchants are adapting by providing easy ways for customers to send back their products: drop off unwanted products in physical stores or directly at home through partnerships with shippers (Colissimo, FedEx…).

75% of products are relisted on an e-commerce website or sold through resellers and liquidators. Many companies are growing in that space in the US, such as the leading auction site liquidation.com, or players like Quicklotz, Optoro or B-Stock that operates online marketplaces for retailers to sell their return or unsold products. Small physical stores are also increasing.

As the buy now, pay later model may be democratized in the next few years, return logistics and resale channels will certainly be new challenges leading to new great market opportunities.

🚀 E-commerce is (still) booming

If 2020 has been a complicated year for lots of businesses, E-commerce has benefited from the crisis. In France, digital sales should reach 110 million euros in 2020 (+6% YoY). This figure actually hides important disparities as home equipment, cultural and leisure products, or sport equipment has shown strong 2-digit growth.

While the pandemic may have affected its activities (supply chain under tension and limitation of activities in certain countries), 2020 should also be a great year for Amazon that realized USD 145 billion dollars of net product sales over the first 9 months of 2020 (+32% YoY).

Regarding Shopify, same cause, same effect, with tremendous growth. Shopify realized 1,9 billion dollars of revenue over the first 9 months of 2020 (+82% YoY), Shopify e-merchants realized 5.1 billion dollars of sales (+76% compared to 2019) during the 3 days Black Friday and Cyber Monday. Beyond the growth of the e-commerce market and the signing of new e-merchants, this overall performance has also been allowed by (i) the rapid adaptation of the offer to retailers as soon as the COVID pandemic began (dedicated template, specific service offering like click&collect, retailers mentoring…), (ii) the expansion of the offer to very large brands (Heinz for example) and (iii) the expansion of the fulfillment network with the acquisition of new logistics sites.

Through our portfolio companies, we are also observing very strong growth rates in 2020 compared to 2019. Early January is traditionally a slow period (after Christmas and before the January sales). Nevertheless, growth is still there, which is probably a sign that some of the consumers who were afraid to buy online have definitely switched.

🆕 What’s next for new digital brands ?

DNVBs has been hype over the last few years. As the cost of customer acquisition has been increasing, and growth more difficult to address, new digital brands are adapting to their market and are progressively transforming their model. The recent interview of the CEO of Thinx, the DNVB of feminine hygiene products, perfectly illustrates the strategy of new brands that we are working on at Spring.

Market: from a niche market targeting a very specific subset of customers, brands are embracing mass-market strategy;

Product: from a vertical approach relying on a single product, news brands are expanding their product lines to leverage their customer base. In the case of Thinx, activewear is now completing the initial product line;

Sales channels: from a pure digital strategy, brands are moving to an omnichannel strategy; an increasing number of new brands are now natively omnichannel as we previously described as the ONVB model (in FR, in ENG); In the case of Thinx, distribution is not only direct e-commerce anymore but also wholesale distribution (through department stores, Amazon…);

Production: DNVBs are well known for their very short production cycle allowed by small series, and a small number of highly selected manufacturers. Like Thinx, most of them are now adding new manufacturers to diversify their production and to increase their volume. Maintaining quality is the new issue ;

Acquisition strategy: paying ads on social networks being highly competitive as big traditional brands are pouring huge amount of money into it, new brands are looking at traditional media (press, radio, TV) as a new way to target a larger base of potential customers ;

Loyalty strategy: social networks are now mostly used by digital brands to engage the community (especially in the COVID period as many people are spending most of their time at home).

DNVBs entered a mature phase where competitive advantage relies on brand awareness more than their initial strengths (digital, vertical, production, disintermediation…). If DNVBs are not Digitally-Native Vertical anymore, they remain Brands and will have to act like it.

❓ Did we enter into the marketplace era ?

Marketplace publishers have multiplied over the last years like Mirakl, the leading platform that raised USD 300 million last September. After competing with Amazon, Cdiscount announced this week that it will launch a Mirakl-like solution for e-merchants. This solution allows merchants to create and operate their own marketplace. But Cdiscount also offers additional services like access to all products sold on cdiscount.com, a complete fulfillment service, and operational support to operate marketplaces. On the B2B side, Wizaplace is doing a great job at its own pace.

In just a few years, marketplaces became the new must-have for distributors that want to extend their e-commerce activity. Is this trend sustainable ?

One of the rules of physical retail says that you need full shelves to make people buy your products. Another rule says that the more products you have in stock, the more you will sell. Marketplaces finally provided a solution to address these points for digital sales by extending product lists to infinity and helping distributors to leverage their community of suppliers.

However, if we try to look forward to this booming market, we may wonder how all these marketplaces will differentiate as customer experience, products and suppliers tend to be the same. On the customer acquisition side, with an increasing dependence on platforms such as Google or Facebook that actually own the customer, differentiation is not that easy. Verticalisation, additional services completing the product offer, or ecosystem animation, could be part of the solution. If nobody knows how this market will evolve, we can be sure that if an e-merchant fails to operate a profitable e-commerce business because of the increasing cost of customer acquisition, the marketplace will not help but will probably make the situation worse.

👍 If you like Retail Chronicles and want to help it grow, please share this newsletter with your colleagues, followers, and friends. If you hate it, then send it to your enemies. Have a great day, and see you soon!

About us

Spring Invest is a French investment fund dedicated to companies that are shaping the future of retail. We invest both in Enablers, B2B companies providing innovative solutions to (e)retailers and brands, and Disrupters creating new models of distribution. Our investment approach relies on strong relationships with 50+ European Retailers and Brands in order to provide sales acceleration to our portfolio. We also provide operational support with a dedicated team of Venture Partners working with our portfolio on sales, communication, HR, and internationalization.