Retail Chronicles | 23.11.2020

Retail Chronicles | 23.11.2020

Emerging trends in retail and new commerce.

Hello, it’s Laurent from Spring Invest, a French investment fund dedicated to RetailTech. Welcome to the latest edition of Retail Chronicles, our bi-monthly newsletter about emerging trends in retail, brands, and new commerce.

🚚 Urban Logistics is on fire

👉 What if malls became new urban logistics hubs?

Last summer, Simon Property Group reported that they were talking with Amazon to offer vacant department stores as fulfillment centers. With 100 fulfillment centers across the US, Amazon is looking to increase its territorial coverage to better compete with Walmart (4.800 stores) or Target (1.800 stores). At the same time, they were announcing their partnership with the US Logistics-as-a-Service platform startup Fillogic to launch multiple tech-enabled micro-distribution hubs.

Last week, Takeoff Technologies, a US startup providing automated grocery micro-fulfillment solutions that can be placed in all small spaces reported that they were working with a large European mall operator with hundreds of locations to convert empty commercial spaces into mini-fulfillment centers.

Malls characteristics (standardized warehouse-sized spaces, central locations, loading docks, on-site retailers) could make them the missing link in the last mile logistics chain as a third-party fulfillment and logistics provider.

👉 Dark stores as an answer to last-mile delivery efficiency

To address the issue of efficient last-mile delivery, Glovo, a Spanish startup, launched Q-commerce, a new delivery service relying on Glovo Market, a business unit that plans to open 100 dark stores (these are warehouses or distribution centres set up with products for online shopping only) by the end of 2021 in Spain and Italy. Such approach will allow Glovo to deliver groceries, toys, books, flowers, or beauty products in less than 30 minutes in major cities.

👉 “New era of retail”, Walmart’s omnichannel strategy

Walmart announced that it will use 4 of its US stores as hybrid centers operating both as shopping destinations and online fulfillment hubs. 2 such hubs are already up and running, while the remaining 2 are set to open soon. These experiments rely on process optimization and technologies:

Omni-assortment: categories that are hard to manage are removed online;

Inventory speed: proprietary solution using Augmented Reality that helps employees getting items quicker from back shop to sales floor;

First-time pick rate: a combination of in-store signage and handheld devices to optimize picking in warehouses;

Checkout experience: new software and hardware solutions for a contact-free checkout.

If the tests go well, this new model will be integrated into Walmart's omnichannel strategy, giving them a definite advantage in terms of territorial coverage with its 4.800 stores.

🧱 M&A with Amazon Seller Companies is booming

Empire Flippers, Thrasio, Perch, Boosted Commerce, Heroes are their name. Consumers do not know them. However, these companies are selling several thousand products on Amazon and their valuation ranges from a few hundred million to a billion dollars. They all are recent companies.

These new companies raised lots of money from VC funds to build a diversified portfolio of Amazon sellers. They are buying the Amazon account and the IP address of a seller that is generating between 1 and 5 million euros a year. Then they plug it into their own logistics, legal, marketing, and creative teams to turn already successful Amazon products into real hits. The valuation of an Amazon Seller typically ranges from 3x to 4,5x its net profit. The typical acquirer portfolio is made of home and DIY products, cleaning products, clothing as well as products for children and pets.

More detail on this amazing sector in the original paper written by Michael Waters, a journalist at Modern Retail.

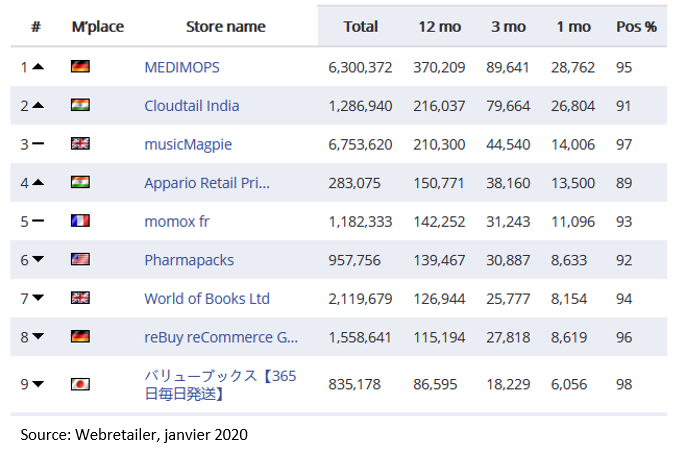

Also, a list of the top Amazon sellers per country is available here.

🚀 Alibaba Singles Day 2020

Alibaba Singles Day 2020 took place on 11/11. Like every year, numbers are staggering:

14 million products, 250.000 brands, 800 million customers, 89 countries;

€62.9 billion of revenue generated in 4 days (vs €32 billion in 2019 on a single day);

2.32 billion orders (vs 1.29 in 2019) with a peak at 583.000 orders in a single second;

13 brands each generated more than €128 million of revenue;

474 brands each generated more than €13 million of revenue (Apple, L’Oréal, Haier, Estée Lauder, Nike, Huawei, Midea, Lancôme, Xiaomi, Adidas…);

16 electronic brands made €13 million of revenue each in a single hour;

US brands represent 14% of total sales;

For this 2020 edition, Alibaba made several new experiments:

200 luxury brands (Montblanc, Cartier…) were invited to join 11/11;

A live-streaming platform was set-up for brands to promote their products through influencers. As an example, Cartier realized 400 live streams;

Cainiao, the logistics arm of Alibaba, committed to only use biodegradable packagings, and half of them without tape;

Alibaba encourages Chinese consumers to drop off their packagings at one of the 80.000 recycling points across China.

Cainiao now has to ship hundreds of millions of packages all over the world throughout the next few days.

French Black Friday generated €6 billion of revenue in 2019. The 2020 edition will start on 4/12 and is particularly awaited this year by (e-)merchants.

🥊 The battle between traditional brands and D/ONVBs is biased

In a recently published paper, Fred Cavazza explains why the battle between traditional brands and new digital -or omnichannel- native vertical brands is asymmetrical.

Traditional brands are actually store-based, while DNVBs are data-based.

Although some of the traditional brands tried a direct-to-consumer approach, most of them are distributed through retailers and therefore do not have any direct link with customers. They depend on the data that retailers are willing to share with them. Those traditional brands no longer have budgets to order customer or market studies.

On the other side, DNVBs/ONVBs are able to collect all the data they need to optimize their operations as they internalized all the value chain (conception, marketing, advertising, PR, distribution, customer relations…) and are selling directly to their end customer.

If both legacy brands and DNVBs are adopting an omnichannel approach, the latter’s enhanced customer knowledge seems to grant them a significant advantage.

Read the full paper (in French) here.

👍 If you like Retail Chronicles and want to help it grow, please share this newsletter with your colleagues, followers, and friends. If you hate it, then send it to your enemies. Have a great day, and see you soon!

About us

Spring Invest is a French investment fund dedicated to companies that are shaping the future of retail. We invest both in Enablers, B2B companies providing innovative solutions to (e)retailers and brands, and Disrupters creating new models of distribution. Our investment approach relies on strong relationships with 50+ European Retailers and Brands in order to provide sales acceleration to our portfolio. We also provide operational support with a dedicated team of Venture Partners working with our portfolio on sales, communication, HR, and internationalization.