Retail Chronicles | 08.12.2020

Retail Chronicles | 08.12.2020

Emerging trends in retail and new commerce.

Hello, it’s Alexandre from Spring Invest, a French investment fund dedicated to RetailTech. Welcome to the latest edition of Retail Chronicles, our bi-monthly newsletter about emerging trends in retail, brands, and new commerce.

💡 Shopify vs. Amazon : a dive into the merchant’s side

The story of the last 20 years in e-commerce has been about Amazon’s rise, from a humble reseller of books to a default shopping destination. On the customer’s side, this is no secret that its success lies in convenience as the care of Amazon towards its customers has benefited both of them with perfect end-to-end experience and to Amazon, securing its dominance. On the merchant’s side, 1.7 million have signed up since Amazon first opened up its marketplace in 1999 to third-party sellers, now accounting for about 60% of the commercial activity on Amazon.

PROBLEM : Merchant’s proliferation has, paradoxically, undercut what power they can exert. Individually, they have little brand recognition and little negotiating power against the marketplace.

The story of Shopify’s rise, then, is in many ways a reaction to Amazon’s :

If the key to Amazon’s success has been to put the customer first, for Shopify the key has been to put the merchant first.

As a reminder, Shopify was founded in Canada in 2006 as a simple maker of e-commerce websites : store owners could upload pictures of their products, set prices, provide their bank account information and start selling. 15 years later, Shopify is the No. 2 player in US e-commerce, powering 6% of sales (compared to Amazon driving 37%) and a market capitalization exceeding $100 billion. In Q3 2020, Shopify’s GMV was $30.9 billion (more than 2x what it was a year ago). About a million merchants use the platform, most of them being SMBs that pay $29 a month for the basic software. More than 7,000 Shopify merchants subscribe to Shopify Plus (a premium version that enables much more customization), now accounting for 25% of Shopify’s MRR.

BUT WHAT DOES SHOPIFY REALLY MEANS TO MERCHANTS ?

Besides turning e-commerce software into a commodity, Shopify brings many things to the table from a merchant’s perspective :

➡️ CUSTOMER RELATION - If you are playing the long-term, building a true customer relationship is at the essence of any commerce business. While Amazon is bypassing the brands by building this relationship itself (you buy from Amazon, not from the seller), Shopify is by design a low-profile tool that lets the merchants do it by themselves, therefore controlling it. This is why Shopify played an outsize role in fueling the DTC era as the whole spirit of these brands is owning the relationship with the customer, having a direct line. Saying it differently, “Shopify is about a new generation of e-commerce merchants who want a shot at securing control by going out on their own”.

➡️ BRAND IDENTITY - For many brands, what is being sold is not just some product with utility. It’s a feeling, a community, and an identity. Shopify, being the blank canvas it is, is much more suitable for this kind of projection than Amazon, which, by virtue of being Amazon, effectively eclipses individual brands on its site. As an example, Allbirds (one of Shopify’s biggest merchants) still avoid selling through Amazon, despite the fact that doing so would be a shortcut to growth. The hits Allbirds would take to the integrity of its brand and pricing power aren’t worth it to the company. Allbirds’ CEO even said that “Amazon is designed to commoditize products to the lowest common denominator of what they stand for. They would love to devolve us into a feature-and-benefit set and then put every knockoff in the world next to us”.

➡️ SERVICES - In addition to providing the software itself, Shopify has been expanding its offerings around merchant’s needs : logistics, financing, checkout, return and refund management, etc. For Shopify’s CEO, the mission is clear “If Amazon is trying to build an empire, Shopify is trying to arm the rebels”. As for logistics, Shopify introduced earlier this year Shopify Fulfillment Network, a direct competitor to Fulfillment by Amazon. However, instead of building or taking over its own warehouses, it created a network of existing third-party logistics providers and retrofitted their software and hardware to closely integrate it with the Shopify platform. For merchants, it means a much more unified offline-online experience. On the other side, they would still rely on the quality of execution of their logistic providers to compete with Amazon’s excellence.

➡️ A VIRTUOUS ECOSYSTEM - Shopify has successfully built a true ecosystem for developers on top of its platform. In fact, Shopify provides 80% of the features that merchants need and third-party developers supply the rest by building customized apps (reviews, discount, SEO plug-in, subscription management, etc.). Therefore, while Shopify made a billion dollars in revenue last year, Shopify app developers made almost $7 billion as a community. The better developers serve the merchants, the more they make money, creating a true win-win-win situation for merchants, developers, and Shopify.

NOW, WHAT ?

While there are many advantages of using Shopify instead of Amazon, it also comes at a huge price : TRAFFIC. Indeed, while Amazon’s merchants benefit from its unparalleled traffic, Shopify’s merchants are on their own to build it, therefore the endless acquisition cost question. In his battle against Amazon, Shopify’s next billion $ question is How can we help merchants to drive traffic while not becoming an Amazon-like marketplace ?

Shopify announced in May a partnership with Facebook Shops to provide exactly that : a simple solution to buy traffic for merchants (more about Facebook Shops below). Shopify also announced a partnership with Walmart.

Read more about the competition between Amazon and Shopify here. On a directly related topic, here is more about the competition between Amazon and traditional retailers.

🛍 Facebook’s commerce ambition

Last week, Facebook reached an agreement to buy Kustomer, a startup focused on customer service technology and chatbots. Terms weren't disclosed, though the Wall Street Journal said it valued Kustomer at $1 billion.

As a reminder, Kustomer's platform provides a single-screen view of conversations between businesses and consumers among different channels (phone, email, webchat, and messaging) to help customer service agents minimize repetitive tasks.

WHAT IS TO LEARN FROM THAT ?

➡️ ADAPTING TOOLS TO SOCIAL-MEDIA COMMERCE. As more people use Instagram, Facebook, or WhatsApp to buy items, it also increases the likelihood that they are going to want to use those apps to communicate with a company during and after a transaction. In fact, we know that 79% of consumers get frustrated when they can't contact customer service on their preferred medium or platform. We will probably see more and more brands moving to customer’s preferred medium for the entire relationship (advice, checkout, delivery updates, support, loyalty programs, etc.), and Kustomer is here to help merchants manage this transition.

➡️ IN-APP CATALYST ARE REQUIRED. This acquisition comes at a time when Facebook is trying to get people to buy more through its various apps like Instagram Checkout and Shops. But getting people to buy more doesn’t just depend on just making it easier for people to enter their credit card number. It also depends upon convincing e-commerce companies to turn to Facebook for more of the necessary services to facilitate a transaction, including customer service.

➡️ THE BATTLE FOR THE RELATIONSHIP - Interestingly, the launch of Checkout shows that Facebook started to take on more responsibility for other parts of the buying process. For example, with Checkout, Facebook sends order and shipping confirmation emails to the customer, and not the company the customer is buying from. However, one of the biggest factors affecting the growth of Checkout is the fact that brands have to give up some control over their relationship... As always, the key in commerce is to own the relationship with customers, and once again, the battle between Facebook and brands is no exception.

Read more here (Modern Retail), here (Retail Dive), here (L’Usine Digitale)

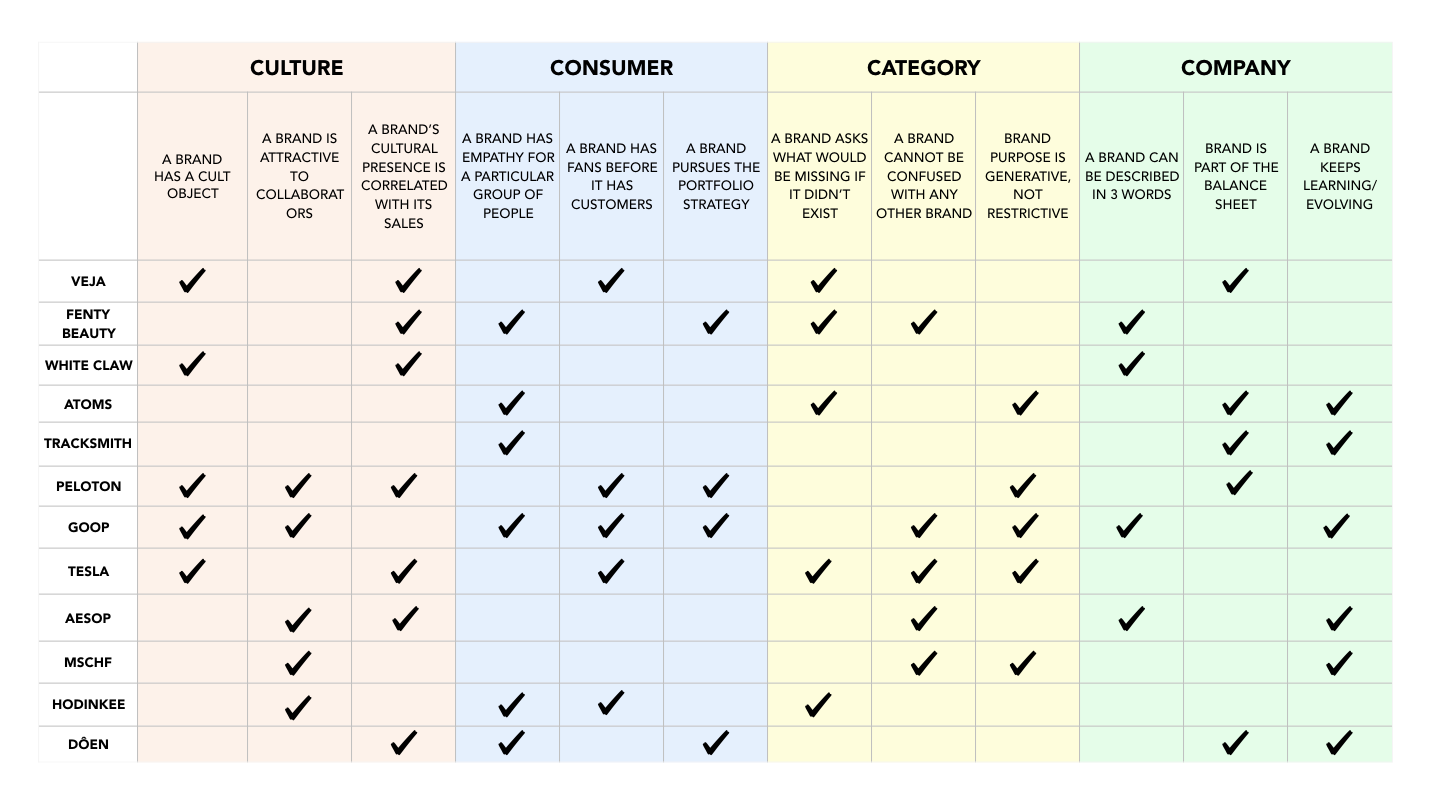

✔️ The Brand Checklist

In this excellent article, Ana Andjelic is evaluating a sample of brands according to the set of 12 criteria grouped into 4 segments : Culture, Consumer, Category, Company.

As a reminder of her last post, this is what the 4 segment means :

CULTURE refers to the emerging social, cultural and political values; it also refers to definition of the core social terms (e.g. influence, community, taste, equality, aspiration); mood, attention and vocabulary.

CONSUMER refers to how well a company can define and understand who its consumer is and the context they make decisions; what they pay attention to and what they spend money on; what they value and expect from the world and each other.

CATEGORY refers to the existing playbook of brand growth in a specific vertical and explores how to capitalize on its strengths and limitations.

COMPANY refers to the 1+1=3 of a company’s team, culture, processes, organization and workplace dynamic. It looks into the social and cultural capital of its founders and the leadership team, the size and composition of their network, and alignment between internal and external cultures.

➡️ The idea of this checklist is to go beyond the usual signals which prioritize rapid financial growth and short-term brand differentiation, offering a comprehensive view with a more diverse set of measures to evaluate a brand’s long-term staying power.

➡️ At Spring Invest, we believe that the challenge for this new consumer brand generation is first and foremost to make their initial differentiation a durable advantage, which can take several forms: product-led durability, community-led durability, and distribution-led durability.

📦 Micro-fulfillment center

In the middle of the COVID-19 pandemic, there have been many talks about converting retail space into micro logistic centers. More recently, Pepsi even launched its first micro-fulfillment center, “providing COVID-19 safety, reducing the costs of floor space, expediting the picking process, allowing for faster delivery and a reduction on overall delivery costs”

A few months later, it does not seem to be such a good idea anymore :

ECONOMIC - Reconverting retail space into logistics space comes in at a high price, being more expensive than repurposing that same space into apartment buildings or offering it to other retailers.

POLITICAL - Political barriers include restrictive zoning and community opposition to projects. Urban retail space is often located near residential space, further complicating the issue.

PHYSICAL - Physical obstacles such as poor reconfigurability of existing structures, inefficient site layouts, and space constraints make it complex for conversion plans to succeed. Quite frequently, retail spaces aren’t normally big enough to serve as distribution centers.

👍 If you like Retail Chronicles and want to help it grow, please share this newsletter with your colleagues, followers, and friends. If you hate it, then send it to your enemies. Have a great day, and see you soon!

About us

Spring Invest is a French investment fund dedicated to companies that are shaping the future of retail. We invest both in Enablers, B2B companies providing innovative solutions to (e)retailers and brands, and Disrupters creating new models of distribution. Our investment approach relies on strong relationships with 50+ European Retailers and Brands in order to provide sales acceleration to our portfolio. We also provide operational support with a dedicated team of Venture Partners working with our portfolio on sales, communication, HR, and internationalization.